Data Insight: What Comes Next for the “Capital of Capital”

By ; Bakinam Khaled

GPCA’s Research team examines the Middle East’s reemergence as a key private capital market in 2025 and outlook for 2026 and beyond in the wake of the Iran conflict.

The US and Israel’s military conflict with Iran has disrupted supply chains, damaged energy infrastructure and introduced a new wave of uncertainty for private capital investors in the Middle East. Nonetheless, new announcements from global fund managers are signaling sustained commitment to the region following a record 2025 for fundraising and investment activity.

In March 2026, Brookfield reaffirmed its plans for a USD20b AI joint venture in Qatar and select international markets, stating that the war is not expected to derail the project. Hong Kong-based Gaw Capital secured a USD150m initial close in March for its inaugural USD400m GCC fund and announced new offices in Abu Dhabi and Riyadh.

Blackstone also led a USD250m investment in UAE-based Advanced Digital Gaming Technology. The latest deals build on a multi-year shift among GPs from viewing the Middle East primarily as a source of LP capital to a core destination for deployment.

2025: A Standout Year

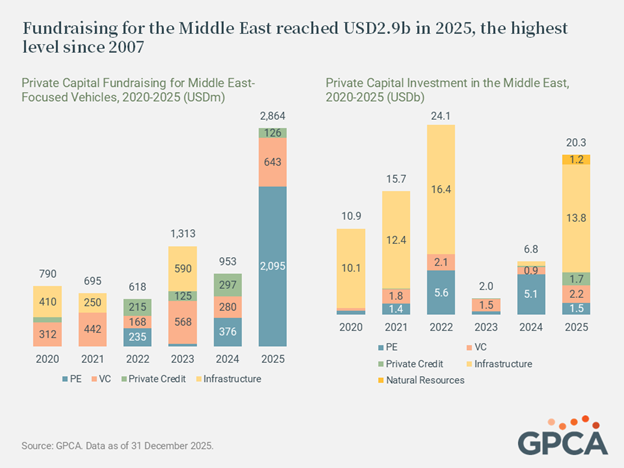

Private capital deal value in the Middle East reached USD20.3b in 2025 – with key deals across fintech, consumer digital platforms, energy and natural resources – including Orion Resource Partners, DFC and ADQ’s USD1.8b investment into critical minerals consortium Orion Abu Dhabi. Middle East-focused fundraising totaled USD2.9b in 2025 – the highest level for the region since 2007.

A new cohort of local managers, including BlueFive Capital, launched funds supported by local sovereigns and family offices, while experienced global fund managers such as KKR, Apollo and BlackRock deepened their regional commitments.

The Growing Role of Local Investors

Even before the war, local LPs – led by sovereign wealth funds (SWFs) such as Mubadala, PIF, SVC and ADQ – were fueling regional fundraising, accounting for 82% of commitments to Middle East-focused funds since 2019. The conflict in Iran has driven SWFs to shift their interest inward to support local businesses and markets, with PIF recently announcing a decrease in international allocations from 30% to 20%. Private capital’s role could even extend to shoring up security across the GCC, evident in BlueFive Capital’s recent launch of a USD3b defense-focused regional PE fund.

Global GPs’ Expanding Presence

Favorable policies and incentives across the region are driving leading international firms to establish a local presence and increase deployment in the GCC, with investors based outside the region accounting for 51% of named participants in big-ticket deals (USD100m or greater). Global firms have also announced dedicated fundraising initiatives targeting the region, with notable launches including BlackRock’s USD1b Middle East infrastructure fund, Brookfield’s USD2b Middle East Partners and I Squared’s Middle East-dedicated infrastructure strategy.

Regional financial centers, like ADGM and DIFC, are playing a key role in attracting foreign capital. QIA has launched a USD3b FoFs program that will act as an anchor LP for firms with a meaningful local presence. In April 2026, under this program, Speedinvest announced the launch of its MENA flagship fund, backed by Mubadala Investment Company, QIA and EIB.

Saudi Arabia is pursuing a similar strategy to advance its Vision 2030 goals. The Regional Headquarters (RHQ) Program offers incentives such as 0% corporate tax, withholding tax exemptions, support for office setup, talent acquisition and fast-tracked regulatory approvals – attracting firms like KKR and General Atlantic. In April 2026, despite the war in Iran, foreign firms like Barings and Bain Capital announced office openings in the region.

As global managers continue to deepen their footprint by establishing offices in key regional financial hubs, they increasingly lead the region’s most notable transactions. For example, the largest deal of 2025 was a GIP-led USD11b investment in Saudi Arabia-based Jafurah Midstream Gas Company.

International firms are also backing the region’s late-stage tech-enabled companies. Saudi Arabia-based fintech Tamara secured USD1.4b from Apollo, Citibank and Goldman Sachs, while UAE-based proptech Property Finder raised USD525m from Blackstone and Permira.

The Digital Drive

As Middle Eastern economies accelerate diversification away from oil and gas, investor attention, both local and global, has increasingly shifted toward AI and related digital infrastructure – a key policy pillar for initiatives like Saudi Vision 2030. According to a recent PwC report, AI could contribute approximately USD320b to the Middle East economy by 2030. The UAE is expected to capture the largest relative benefit, with AI potentially contributing close to 14% of GDP.

Saudi Arabia and the UAE are currently leading the region’s digital buildout, attracting significant commitments from international fund managers in partnership with local sovereign wealth funds and corporates. Notable examples include G42, MGX and Silver Lake’s USD2.2b investment in the UAE-based data center Khazna. Similarly, global tech leaders announced plans to build data center infrastructure in the Middle East, including AWS’s USD5.3b investment in Saudi Arabia, Microsoft’s USD1.5b investment in the UAE and OpenAI’s plans to develop a 1-gigawatt AI data center in Abu Dhabi.

These infrastructure investments have continued into 2026, with HUMAIN and Saudi Arabia’s National Infrastructure Fund announcing a USD1.2b strategic financing framework to build 250MW of data center capacity in Saudi Arabia.